If you’ve ever asked “term vs whole life insurance — which one should I buy?” and gotten five different answers from five different agents, you’re not alone. The truth is, both products are tools. Each one solves a different problem. The right choice for your family depends on your goals, your budget, and what stage of life you’re in. We’ll break down the real differences in plain English, share who each one is best for, and help you walk away knowing exactly which direction makes sense for you.

Table of Contents

Term vs Whole Life Insurance: The Quick Answer

Here’s the short version before we dig in:

- Term life insurance covers you for a set period — usually 10, 20, or 30 years. It’s affordable, simple, and built for income replacement during your highest-responsibility years.

- Whole life insurance covers you for your entire life and builds cash value over time. It costs significantly more but doubles as a long-term financial tool.

For most young families, term life insurance is the right starting point. For people focused on estate planning, business protection, or tax-advantaged wealth building, whole life can play a role. Let’s get into the details.

How Term Life Insurance Works

Term life is the simplest form of life insurance. You pick a coverage amount (say, $500,000), pick a term length (say, 20 years), and pay a monthly premium. If something happens to you during that term, your family receives the death benefit tax-free.

If the term ends and you’re still here, the policy expires. You can renew, convert it to permanent coverage, or let it go.

Who term life insurance is best for:

- Young families with kids at home

- Homeowners with a 15–30 year mortgage

- Anyone whose family depends on their income

- People looking for the most coverage for the lowest monthly cost

Pros of term life:

- Affordable. A healthy 35-year-old can often get $1 million in 20-year term coverage for under $50 a month.

- Simple. No cash value, no investment component, no fine print.

- Flexible terms. Pick a length that matches your highest-risk years (until kids are grown, mortgage is paid).

Cons of term life:

- Coverage ends when the term does

- No cash value or investment buildup

- Premiums increase if you re-buy after the term expires (because you’re older and possibly less healthy)

How Whole Life Insurance Works

Whole life is permanent coverage that lasts your entire life — as long as you keep paying premiums. A portion of every premium goes toward the death benefit, and another portion goes into a cash value account that grows tax-deferred over time.

You can borrow against the cash value or withdraw from it during your lifetime. According to Investopedia, whole life policies typically include guaranteed minimum interest growth on the cash value portion.

Who whole life insurance is best for:

- People with significant assets who want estate planning protection

- Business owners using policies for buy-sell agreements or key person coverage

- Parents wanting to lock in lifetime coverage for a child while young and healthy

- Higher-income earners who’ve maxed out other tax-advantaged accounts

Pros of whole life:

- Lifetime coverage. Never expires as long as you pay premiums.

- Cash value buildup. Grows tax-deferred and can be borrowed against.

- Fixed premiums. Lock in your rate at today’s age and health.

- Estate planning tool. Death benefit passes to heirs income-tax-free.

Cons of whole life:

- 5–15× more expensive than term for the same coverage amount

- Cash value grows slowly in early years

- Less flexibility than other investment vehicles

- Many people don’t need lifetime coverage

Term vs Whole Life Insurance: Cost Comparison

Here’s a real-world example. A healthy 35-year-old non-smoker buying $500,000 in coverage might pay:

- 20-year term: ~$25–$35 per month

- Whole life: ~$400–$500 per month

That’s roughly 15× the cost. For most families on a budget, term wins because it lets you buy enough coverage to actually protect your family without breaking the bank.

Term costs a fraction

of whole life.

A healthy 35-year-old non-smoker buying $500,000 in coverage faces a stark price gap. Here’s what those monthly premiums actually look like, side by side.

Monthly premium, to scale

roughly

Term Life

- 01Lowest cost. Premiums stay level for the full 20-year term.

- 02Buy more coverage. Same budget unlocks 10–20× the death benefit.

- 03Simple. No cash value, no investment component, no surprises.

- 04Expires. Coverage ends when the term ends — by design.

Whole Life

- 01Lifetime coverage. Never expires as long as premiums are paid.

- 02Builds cash value. A portion accumulates tax-deferred over time.

- 03Fixed premium. Locked for life, but starts ~15× higher.

- 04Complex. Fees, dividends, and surrender charges to read carefully.

Want to see what your real number should be before comparing policy types? Use our free life insurance calculator to find your personalized coverage amount in under two minutes.

The “Buy Term and Invest the Difference” Strategy

You may have heard financial pros recommend “buy term and invest the difference.” The idea: buy affordable term coverage to protect your family during the years you need it most, and invest the money you’d otherwise spend on whole life premiums in a 401(k), IRA, or other tax-advantaged account.

For most people, this strategy outperforms whole life over the long run because:

- You get the same income protection during the term

- Your investments typically grow faster than whole life cash value

- You have more flexibility with your money

The catch? You actually have to invest the difference. If you buy term and spend the savings, you’re left with no coverage and no nest egg. Discipline matters.

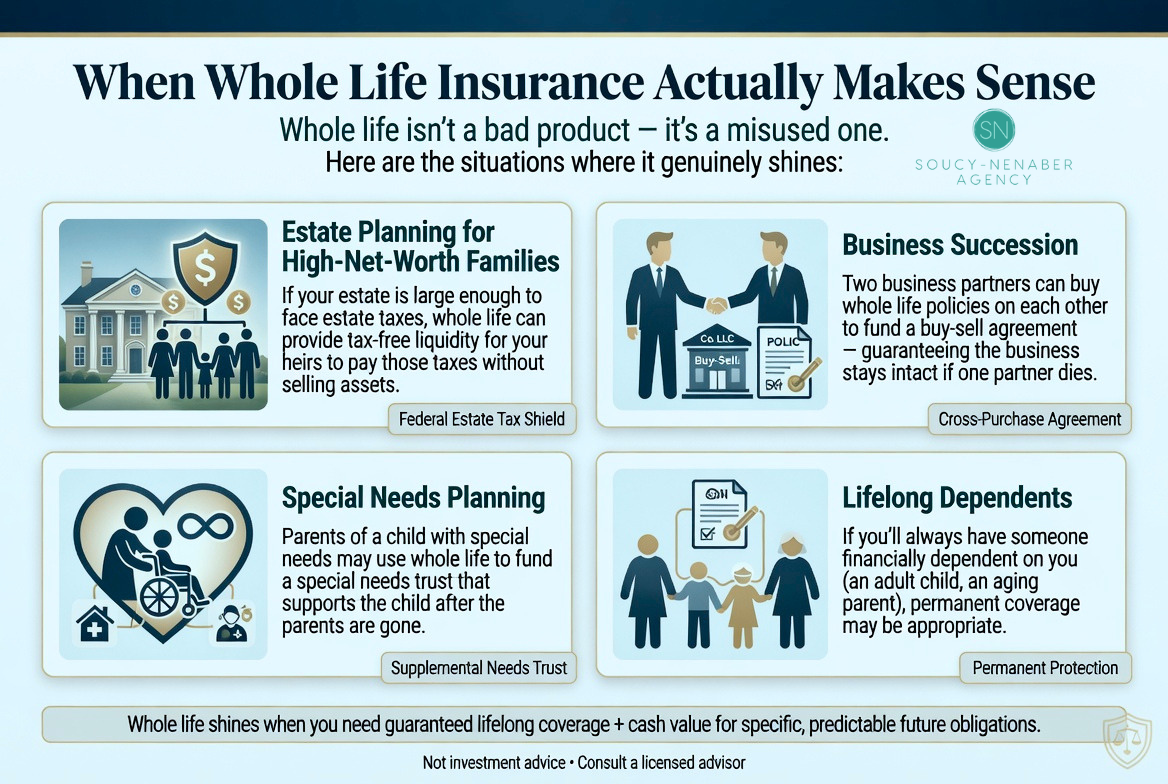

When Whole Life Insurance Actually Makes Sense

Whole life isn’t a bad product — it’s a misused one. Here are the situations where it genuinely shines:

Estate planning for high-net-worth families

If your estate is large enough to face estate taxes, whole life can provide tax-free liquidity for your heirs to pay those taxes without selling assets.

Business succession

Two business partners can buy whole life policies on each other to fund a buy-sell agreement — guaranteeing the business stays intact if one partner dies.

Special needs planning

Parents of a child with special needs may use whole life to fund a special needs trust that supports the child after the parents are gone.

Lifelong dependents

If you’ll always have someone financially dependent on you (an adult child, an aging parent), permanent coverage may be appropriate.

How to Choose Between Term and Whole Life Insurance

Ask yourself these questions:

- How long will my family depend on my income? Until kids graduate? Until the mortgage is paid? That’s your term length.

- What’s my budget? If you can only afford one or the other, prioritize coverage amount over policy type. A bigger term policy beats a smaller whole life policy every time.

- Do I have estate or business needs? If yes, ask an agent about layering term + whole life.

- Have I maxed out my retirement accounts? If you haven’t filled your 401(k) and IRA, whole life is rarely the smartest place for extra dollars.

For 80% of families, the right answer is a strong term policy with a coverage amount that matches your real needs (use the DIME calculator to find that number).

Frequently Asked Questions

Q: Is whole life insurance ever a good investment?

A: It’s better thought of as a financial tool than an investment. For high-income earners who’ve maxed out retirement accounts, business owners, and people with estate planning needs, whole life can serve a purpose. For most families, term life plus a 401(k) outperforms whole life over the long run.

Q: Can I switch from term to whole life later?

A: Yes — most term policies include a conversion option that lets you convert some or all of your coverage to whole life without a new medical exam. This is a great option if your situation changes mid-term.

Q: What happens to whole life cash value when I die?

A: This is the big surprise for most people: with most whole life policies, the insurance company keeps the cash value when you die. Your family receives only the death benefit. There are policies that pay out both, but they cost significantly more.

Q: Should I buy term life insurance through my employer?

A: Employer-provided life insurance is a nice perk, but don’t rely on it as your only coverage. It usually caps at 1–2× your salary, and it disappears the day you leave the company. Buy your own private policy as your primary coverage.

Q: How do I know how much term life insurance to buy?

A: Use the DIME method: add your Debt + Income replacement + Mortgage + Education costs, then subtract existing coverage and savings. Or skip the math and use our free calculator — it does it for you. https://snagencylife.com/free-life-insurance-calculator/

The Bottom Line

Term vs whole life insurance isn’t a debate about which one is “better” — it’s about which one fits your goals. Term wins on affordability, simplicity, and pure income protection. Whole life wins for estate planning, business needs, and lifelong coverage scenarios. Most families should start with a strong term policy that actually matches their coverage needs, and revisit whole life later if their situation calls for it.

Not sure which one fits your life? Book a free 15-minute call with one of our licensed agents — we’re contracted with 30+ top-rated carriers and we’ll walk you through both options in plain English. No pressure. No commission-driven push toward expensive products. Just clear answers.