You’re building something beautiful — a family, a home, a future. And somewhere in the back of your mind, there’s a quiet thought you keep pushing off: What would happen to them if something happened to me?

If you’ve been putting off life insurance for young families, you’re not alone. Between diapers and daycare costs and trying to remember the last time you slept through the night, “research insurance policies” doesn’t exactly top the to-do list. But here’s the good news — it’s probably simpler and more affordable than you think. And taking this one step now can give your family a safety net that lasts for decades.

Let’s walk through everything you need to know — no jargon, no pressure, just the stuff that actually matters.

Table of Contents

Why Life Insurance for Young Families Is So Important

Here’s the reality most people don’t want to think about: if you or your partner passed away unexpectedly, could your family maintain their current lifestyle? Could they stay in the same home? Could your kids still go to the schools you’ve been planning for?

Life insurance replaces lost income. That’s the simplest way to think about it. For young families, that protection is critical because you’re likely in the years where your expenses are highest and your savings are still growing.

A study from LIMRA found that nearly half of American adults say they don’t have enough life insurance. And among those without any coverage at all, the most common reason is that they think it costs too much — even though most overestimate the cost by 3x or more.

The truth? For a healthy young parent, a solid term life insurance policy can cost less than your monthly streaming subscriptions.

Term vs. Whole Life: Which One Makes Sense for Your Family?

This is the question that trips most people up, so let’s break it down simply.

Term life insurance covers you for a set period — usually 10, 20, or 30 years. You pay a fixed monthly premium, and if something happens to you during that term, your family receives the death benefit. It’s straightforward, affordable, and the most popular choice for young families.

Whole life insurance covers you for your entire life and builds cash value over time. It costs significantly more than term, but it has a savings component that grows tax-deferred.

For most young families, term life insurance is the right starting point. Here’s why:

- It covers the years when your family is most financially vulnerable

- Premiums are dramatically lower, freeing up money for other priorities

- You can align the term length with your biggest obligations (mortgage, kids reaching adulthood)

- You can always add or convert coverage later as your needs change

That said, every family is different. Some families benefit from a combination of both. The important thing is to talk to someone who can walk you through your specific situation — not push you toward the most expensive option.

How Much Life Insurance Does a Young Family Actually Need?

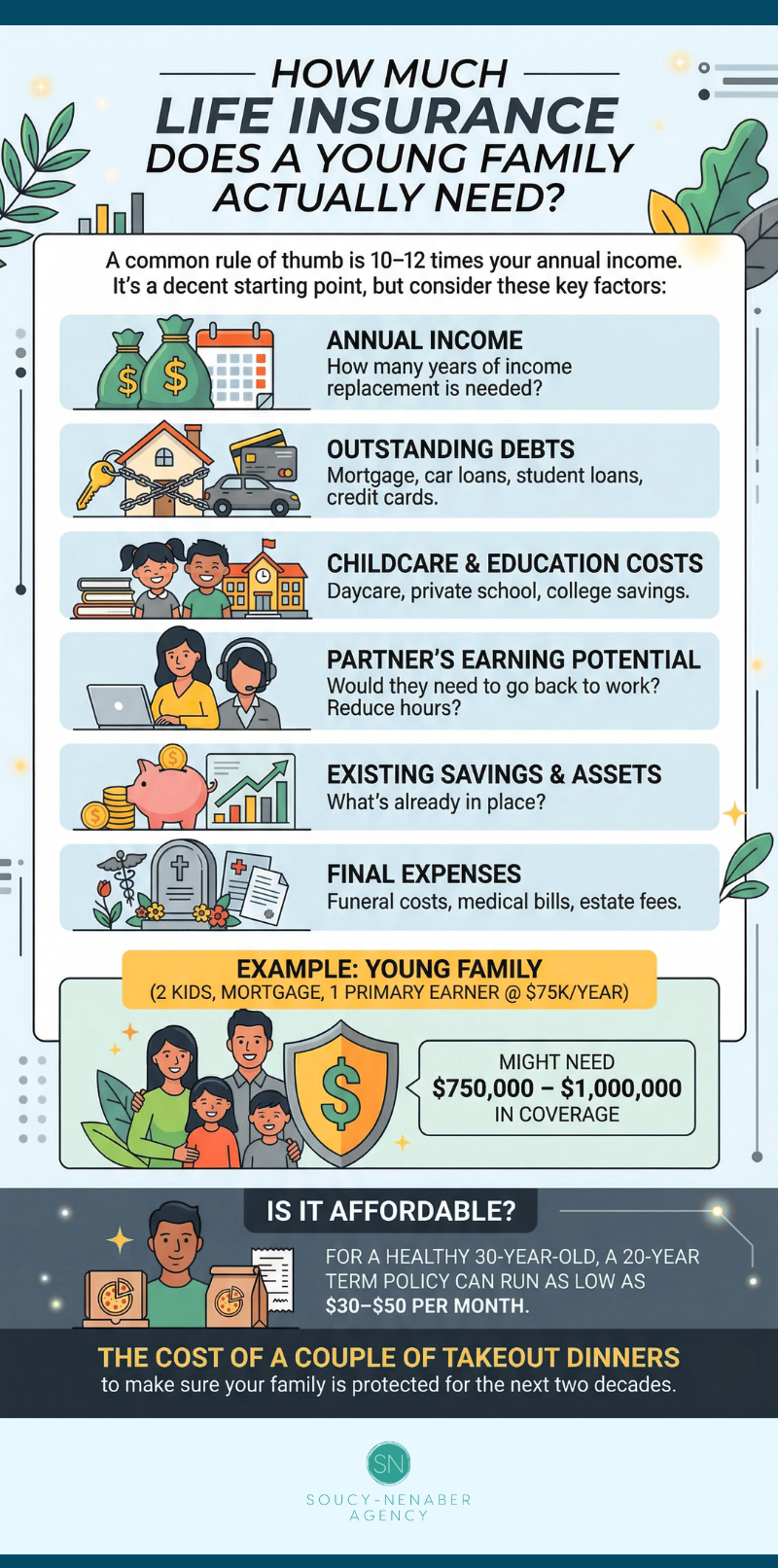

There’s a common rule of thumb that says you need 10–12 times your annual income in coverage. That’s a decent starting point, but it doesn’t tell the whole story.

When figuring out the right amount of life insurance for young families, consider these factors:

- Your annual income — How many years of income replacement does your family need?

- Outstanding debts — Mortgage, car loans, student loans, credit cards

- Childcare and education costs — Daycare, private school, college savings

- Your partner’s earning potential — Would they need to go back to work? Reduce hours?

- Existing savings and assets — What’s already in place?

- Final expenses — Funeral costs, medical bills, estate fees

A young family with two kids, a mortgage, and one primary earner making $75,000 a year might need $750,000–$1,000,000 in coverage. That sounds like a big number, but for a healthy 30-year-old, a 20-year term policy at that level can run as low as $30–$50 per month.

That’s the cost of a couple of takeout dinners — to make sure your family is protected for the next two decades.

When Is the Best Time to Get Life Insurance? (Hint: It’s Now)

The best time to buy life insurance was yesterday. The second-best time is today.

Here’s why waiting costs you — literally:

- Premiums go up with age. Every year you wait, your rate increases. Locking in a policy in your 20s or 30s means significantly lower premiums for the entire term.

- Health changes are unpredictable. A new diagnosis, a change in weight, even a new prescription can affect your rates or eligibility.

- Life moves fast. Once you have kids, buy a home, or take on debt, the stakes get higher — and the cost of being uninsured grows.

If you’ve been telling yourself “I’ll get to it eventually,” this is your sign. Getting covered now — while you’re young and healthy — is one of the smartest financial moves you can make for your family.

Common Myths That Keep Young Families From Getting Covered

Let’s clear up a few things that might be holding you back:

“Life insurance is too expensive.”

For most young, healthy adults, a term life policy costs $25–$50 per month for substantial coverage. That’s less than most gym memberships.

“I get coverage through my job — that’s enough.”

Employer-provided life insurance is a great benefit, but it typically covers just 1–2x your salary, which isn’t nearly enough for a family with a mortgage and kids. Plus, if you leave your job, that coverage goes with it.

“We’re young and healthy — we don’t need it yet.”

That’s exactly why now is the time to buy. You’ll lock in your lowest possible rate and protect your family during the years you’re building the most.

“It’s too complicated to figure out.”

It doesn’t have to be. With the right guidance, you can understand your options and get covered in a single conversation. That’s what we’re here for.

What to Look for in a Life Insurance Agent

Not all insurance experiences are created equal. If you’ve ever felt pressured, confused, or talked into something you didn’t fully understand — we get it. That’s not how it should work.

Here’s what a good agent looks like:

- They listen first. Before recommending anything, they ask about your family, your goals, and your budget.

- They explain things in plain English. No jargon, no fine-print tricks, no making you feel dumb for asking questions.

- They’re non-captive. This means they aren’t locked into one insurance company. They can shop across multiple carriers to find the best fit and rate for you. At SN Agency, we’re contracted with 30+ top-rated carriers across 47 states — so we’re always working for you, not for one company.

- They don’t pressure you. The right policy is the one that fits your life — not the one that earns the biggest commission.

Jamie and Cory Nenaber, the founders of SN Agency, didn’t come from the insurance world. Jamie was a nurse. Cory was in education. They know what it feels like to be on the other side of the table — and they built an agency that treats people the way they’d want to be treated.

How to Get Started With Life Insurance for Your Young Family

Ready to take this off your plate? Here’s how simple the process can be:

- Book a free discovery call. A quick 15-minute conversation to understand your family’s needs and budget. No pressure, no obligation.

- Get a personalized quote. We’ll shop across 30+ carriers to find you the best coverage at the best rate.

- Review your options. We’ll walk you through everything in plain language so you feel confident in your decision.

- Get covered. Most policies can be issued within days. Some don’t even require a medical exam.

That’s it. Four steps between where you are now and the peace of mind that comes from knowing your family is protected — no matter what.

Frequently Asked Questions

Q: How much does life insurance for young families typically cost?

A: For a healthy adult in their 20s or 30s, a 20-year term policy with $500,000–$1,000,000 in coverage typically costs between $25 and $60 per month. Your exact rate depends on your age, health, lifestyle, and the amount of coverage you choose.

Q: Can both parents get life insurance?

A: Absolutely — and it’s strongly recommended. If both parents contribute to the household (whether through income, childcare, or both), losing either one creates a financial gap. Many families get policies for both parents, sometimes at different coverage amounts based on each person’s role.

Q: What happens if I outlive my term life insurance policy?

A: If your term expires and you’re still living (which is the most likely outcome), the policy simply ends. You won’t receive a payout, but you also won’t owe anything. Many people use this as an opportunity to reassess — your kids may be grown, your mortgage may be paid off, and your coverage needs may have changed significantly.

Q: Do I need life insurance if I’m a stay-at-home parent?

A: Yes. Stay-at-home parents provide childcare, household management, transportation, meal prep, and more. Replacing those services would cost the working parent tens of thousands of dollars per year. Life insurance for a stay-at-home parent helps cover those costs if the unexpected happens.

Q: Is it hard to qualify for life insurance?

A: Most young, healthy adults qualify easily. The application process typically involves answering health questions and, in some cases, a brief medical exam. Many carriers now offer simplified or no-exam options that can get you covered in days rather than weeks.

Your family is your everything. And protecting them doesn’t have to be complicated, expensive, or stressful. It just takes one small step — and we’d love to help you take it.

Book your free 15-minute discovery call with SN Agency →

Your future self — and your family — will thank you.